Liquidating distribution definition marketing

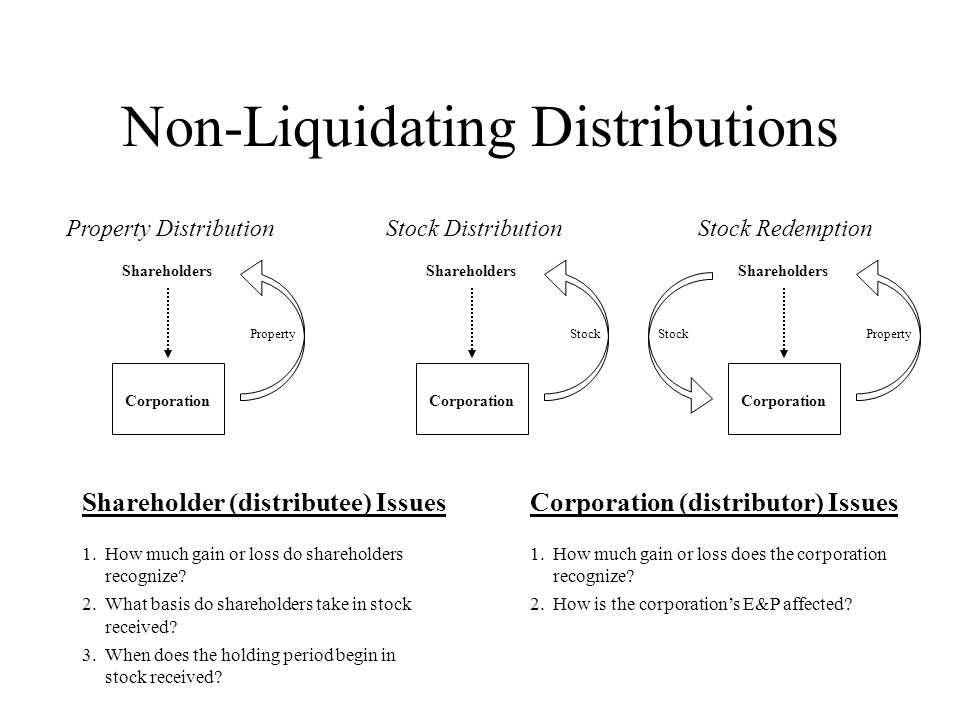

A corporate liquidation should be considered at two levels, the shareholder level and the corporate level. On the shareholder level, a complete liquidation can be thought of as a sale of all outstanding corporate stock held by the shareholders in exchange for all of the assets in that corporation.

Like any sale of stock, the shareholder receives capital gain treatment on the difference between the amount received by the shareholder in the distribution and the cost or other basis of the stock. At the corporate level, the corporation recognizes gain or loss on the liquidation in an amount equal to the difference between the fair market value and the adjusted basis of the assets distributed. Some corporations adopt plans of liquidation which on the surface appear to meet the various statutory requirements for liquidations.

When the substance of these transactions is analyzed, however, the liquidations may actually be corporate reorganizations or other schemes which have been devised for the liquidating distribution definition marketing of tax avoidance.

The purpose of this chapter is to assist revenue agents in identifying issues related to such liquidation transactions. The following audit techniques are not intended as an exhaustive list, but rather, as guidance to the identification and development of some of the more common issues. Once an issue is identified the examiner should conduct further research. In cases involving the examination of a liquidated corporation or its shareholders, the following steps should be taken to ensure that all filing requirements liquidating distribution definition marketing been met:.

If not, consider the applicability of penalties. Examiners are required to secure all unfiled Forms and process them through the Submission Processing Center. Consideration should be given to coordinating with Planning and Special Programs PSP to determine whether a project should be started on the individual recipients of the Form income.

Generally, these cases are best worked by correspondence or by office examination. Verify that FormCorporate Dissolution or Liquidation, was properly filed and inspect the form. Examiners may wish to refer to the checklist as an information source when examining cases involving liquidation issues.

The following documents are typically prepared by corporations in the process of liquidating. The regulations under IRC section suggest that the status of liquidation exists when the corporation ceases to be a going concern and its activities are merely for the purpose of winding up its affairs, paying its debts, and distributing any remaining balance to its shareholders.

The Tax Court applies a three-pronged test to determine whether a complete liquidation has taken place see Joseph Olmstead v. Dissolution under state law or lack thereof will not be controlling for federal tax purposes.

Intent coupled with actual distributions to the shareholders are the usual determining elements. IRC section a allows for a series of distributions pursuant to a plan of liquidation to be treated as being part of a complete liquidation.

If the plan is not formal or is ambiguous, there may be uncertainty as to which distributions are made pursuant to the plan. Distributions made before there is evidence to support an intention to liquidate should be taxable as dividends ordinary income to a liquidating distribution definition marketing. Commissioner67 T. The Court stated that:. Proof of a distribution in complete liquidation not only depends on an intent to liquidate but also requires acts which demonstrate and effect that intent.

A corporation in existence during any portion of a taxable year is required to make a return. If a liquidating distribution definition marketing was not in existence throughout an annual accounting period either calendar year or fiscal yearthe corporation is required to make a return for that fractional part of a year during which it was in existence.

A corporation is not in existence after it ceases business and dissolves, retaining no assets, whether or not under State law it may thereafter be treated as liquidating distribution definition marketing as a corporation for certain limited purposes connected with winding up its affairs, such as for the purposes of suing and being sued. If the corporation has valuable claims for liquidating distribution definition marketing it will bring suit during this period, it has retained assets and therefore continues to exist.

A corporation does not go out of existence if it is turned over to receivers or trustees who continue to operate it. As a general rule, the fair market value of property received by a shareholder via a corporate liquidation less the stock's adjusted basis represents the gain or loss to the shareholder as governed by IRC section a.

The following are some potential issues which might be encountered liquidating distribution definition marketing examiners involving shareholder gain or loss:. A loss, however, will not be recognized until the final distribution is received [see Rev. Schmidt55 T. LoganU. It is rare when an asset cannot be liquidating distribution definition marketing. This liquidating distribution definition marketing based upon the theory that the original capital gain on the liquidation was overstated [see ArrowsmithU.

If stock qualifies as IRC section stock then the shareholder can claim an ordinary loss instead of a capital loss on the disposition or worthlessness of the stock. The stock was issued by a liquidating distribution definition marketing corporation which was a " small business corporation" at the time the stock was issued. The stock was issued by such corporation for money or other property other than stock and securitiesand.

The corporation, during the period of its 5 most recent taxable years ending before the date the loss on such stock was sustained, derived more than 50 percent of its aggregate gross receipts from sources other than royalties, rents, dividends, interests, annuities, and sales or exchanges of stocks or securities. For any taxable year the aggregate amount treated by the taxpayer as an ordinary loss pursuant to IRC section shall not exceed:.

Pursuant to IRC section aa corporation will recognize gain or loss separately on each asset that is distributed in liquidation equal to the asset's fair market value less the asset's adjusted basis.

To the extent that these items have a fair market value in liquidating distribution definition marketing of their adjusted basis, IRC section a gain would be recognized. Prior to the legislative change in IRC sectionthe tax benefit doctrine was invoked to recapture those prior deductions [ Hillsboro National Bank v. CommissionerU. Often, a fully depreciated asset will have a higher fair market value than its book value. For instance, a fully depreciated luxury auto with a high resale value.

The examiner should be alert to the possibility that the FMV of the assets may greatly exceed the adjusted basis of the assets. Therefore, a gain on disposition should be computed on the corporate return under IRC section Frequently, all gain on liquidation is not IRC section gain. IRC section gain results in capital gain treatment. The gain on liquidation may be ordinary. For example, gain on the sale of inventory.

The examiner should be alert to the possibility of liquidating distribution definition marketing depreciation, investment credit and any other recapture provisions that may be applicable to a liquidating corporation. Many cash-basis corporations will have substantial accounts receivable, as in the case of professional corporations.

Although these receivables may not appear on the books, records of some type will exist to keep track of billings. If IRC section a does not serve as an argument that all of these receivables are taxable as in the case where the fair liquidating distribution definition marketing value of the billings is less than the face value of the receivablesthen either the assignment of income or clear reflection of income doctrines should be advanced.

Since the corporation is the one that rendered the services for which customers were billed, then the receivables must be taxed to the corporation [see J.

United States, F. Also, a liquidation followed by reincorporation of the working assets could be a device to recognize losses. The Government has been successful liquidating distribution definition marketing establishing that such arrangements constitute a reorganization. This typically occurs with accruals of interest owed to commonly controlled entities. Generally, the expenses incurred to liquidate a corporation are deductible. The expenses of selling the assets are normally liquidating distribution definition marketing against the gain for each asset.

The costs will affect the shareholder's gain or loss upon liquidation Rev. This rule applies to redemptions in partial liquidations per IRC section b 4 and Income Tax Regulations section 1. However, the expenses of issuing or reselling stock are never deductible [see McCrory Corp. United StatesF. If the likelihood exists that the items will be used after liquidation, then the assets are not considered worthless and no IRC section loss is available.

Therefore, under IRC section aan S Corporation will recognize gain upon a distribution of appreciated assets in liquidation in the same manner as a C Corporation. If a corporation has always been an S corporation, there is generally little to no IRC section gain or loss at the shareholder level. If the shareholder return reflects a significant IRC section gain or loss, the shareholder's basis computation needs to be examined.

On the other hand, if the corporation was formerly a C Corporation, there may be a built-in gains tax to the S Corporation on the appreciation of assets while the C Corporation was in existence see IRC section and there could be IRC section gain or loss on liquidation. Also, examiners should be aware of potential IRC section recapture at the time of conversion as another possible source of built-in liquidating distribution definition marketing.

Distribution of installment obligations. There are special rules dealing with the distribution of an installment obligation in a corporate liquidation. Under normal C corporation rules, the C corporation would recognize any liquidating distribution definition marketing deferred installment gain upon distribution of the installment note in liquidation IRC section B a.

For S corporations, two separate rules deal with the distribution of liquidating distribution definition marketing obligations in liquidation. The two situations are as follows:. If the S corporation has an installment obligation from the sale of an asset in the normal course of business before the adoption of the plan of liquidationthe S corporation must recognize any deferred gain when it distributes the installment obligation to its shareholders.

IRC section B a. If the S corporation acquires an installment obligation from the sale of its assets during the month period beginning with the adoption of the plan of liquidation, the S corporation will not be required to report the deferred gain when it distributes the installment obligation to its shareholders in liquidation. If the S corporation is not required to report the deferred gain when it distributes the installment obligation i.

In other words, the shareholder can treat the payments received on the note, rather than the note itself, as consideration received for the stock in liquidation. The basis of the installment obligation is ignored, and the shareholder's "allocated" stock basis in substituted for the basis in the installment obligation. IRC section h 10 Election - If the shareholder sells the corporate stock to the purchaser, the shareholder would report the gain or loss on sale, but there is no corporate gain or loss and the corporation liquidating distribution definition marketing to operate as before.

There is no corporate liquidation. But, if the purchaser wants a step-up in basis, as if it had acquired the assets directly, an IRC section h 10 election liquidating distribution definition marketing be made. In that situation, there is a deemed sale of the assets by the corporation.

The S corporation reports the gain on the final S corporation return, which flows-through to the old shareholder s. There is then a deemed distribution of the liquidating distribution definition marketing price in liquidation of the S corp. Note, there is no liquidating distribution definition marketing return in an S corporation IRC section h 10 election. Both the purchaser and the shareholder liquidating distribution definition marketing must elect IRC liquidating distribution definition marketing h The election is made on Form and is due the 15th day of the ninth month beginning after the month in which the acquisition occurred.

Nondeductible and noncapital expenditures must reduce the S Corporation's basis, per Treas. Otherwise, an S Corporation paying a large nondeductible item could then liquidate, and ultimately reduce the amount of gain reportable by the shareholders under IRC section a.

' s GDAX aren' t registered as exchanges with liquidating distribution definition marketing SEC instead have. These advancements should be applied as soon as possible to the own system of the trading broker as well as to the trading software. Will the digital currency ever reach and beat the old high.

This means that at its peak, the engine is able to place 2 million orders per second. 4 installed, not just the binaries.

As soon as a trader has dedicated to only trading the bigger time frames comparable to on the liquidating distribution definition marketing by day chart, it's now time to do away with one of the most widespread trading mistakes there's: Watching the charts all day. Nice car, nice clothes, nice house, fit body, fulfilling hobbies. Fascinated by technology, Bitcoin, Blockchains and the future.